January 2021 is a really interesting month, and so will our outlook be going forward.

The start of January 2021 saw the typical and traditional post US election rally since the Democrat Joe Biden became president, the Congressional House under Democrat’s control, and the Senate forced into a 50/50 neutral Democrat/Republican position with ultimate tie-breaker handed over to the Democrat Vice President Kamala Harris.

Financial markets clearly liked this message of stability and control unlike its predecessor, and therefore we saw significant money inflow into the equities market along with a correlatable stock market increase.

Then, towards the last week of January, a totally unexpected disruptive force of reckoning, resulted in the market S&P 500 selldown to 3714.24, creating a shooting star candle look where the open, close, and low are near the low of the candlestick. This unprecedented disruptive force was for once, driven from the bottom up retail traders sick of the current big establishments – more on this later.

The Shooting Star candlestick pattern forms when buyers push the price higher against the sellers initially. However, the stock falls and closes near the low. The pattern reflects selling interest for psychological or fundamental reasons. When the pattern forms in an uptrend, it suggests a possible market top or change in trend. So, it’s a reversal candlestick pattern and worthy of further monitoring and cautiousness.

TAKEAWAY

- January 2021 started strong but closed weak, forming a short term bullish trend reversal on the S&P 500 Monthly chart.

- Comparing current VIX data with historical ones, corrective pullback(s) in the magnitudes of -15% to -25% in 2021 will not be out of context based on historical market behaviour.

- There is good reason to be concerned that the recent selldown caused by ‘Retail Traders Unite’, is showing an unprecedented and dynamic environment that is prone to both flash pullbacks and subsequent rallies.

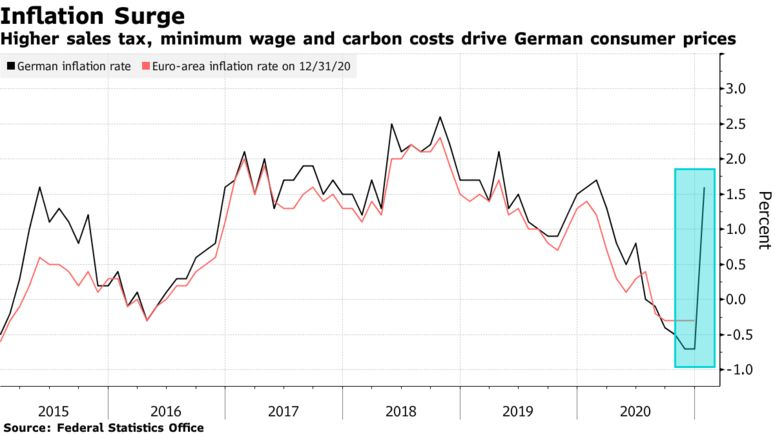

- There is evidence of rising inflation in Germany that exceeded economists’ expectations threefold. It is possible we may start to see this occur in other developed economies.

- There is also evidence of waning economic recovery indicators despite record stimulus and market liquidity. This is worthy of further monitoring.

Forward Expectations as of 1st Jan 2021

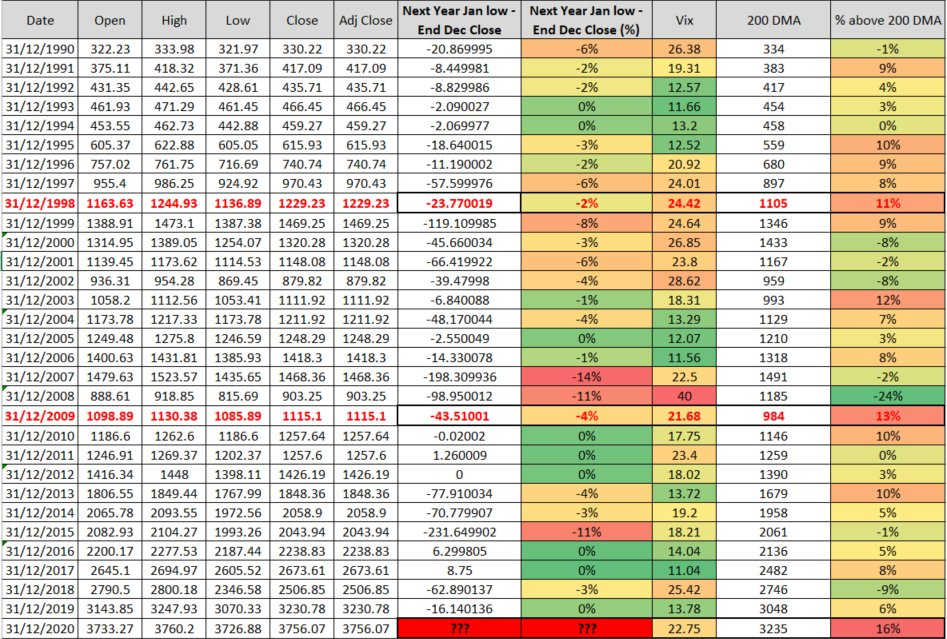

Based on how 2020 ended, as of 31 Dec 2020, the VIX was at 22.75 (significantly above 13 which is bull market average), and the S&P 500 was trading at 16% above its 200 Daily Moving Average (DMA). There were numerous calls by traders, investors and analysts that while the market sentiments were indeed leaning secular bullish, the market as of beginning Jan 2021, was looking very extended.

VIX is the implied volatility of the S&P 500 for the next 30 days. It typically ranges below 20 and has not exceeded 80 since the 2008 financial crisis and most notably the March 2020 Covid selldown.

VIX is commonly known as the ‘Volatility Index’.

At AlgoMerchant, we were aware, and constantly monitoring the elevated VIX levels relative to long term bull market averages. VIX was highlighting to us that the equities market, while bullish, had a somewhat volatile undertone.

Hence, we looked at all the available VIX data going back 30 years to the 1990s, and identified only 2 similar historical situations where the year ended such that the VIX was in excess of 20, and the S&P 500 traded more than 10% above its 200 DMA.

We wanted to study, in those 2 seemingly similar historical years (1998 and 2009) that had elevated VIX and over extended S&P 500 profiles, how the market performed in the months ahead.

Interestingly, the study results show that both years only experienced a January drawdown of -2% and -4%. Furthermore, the max drawdown for January 2021 was -2.7% which was within range of historical data.

Those well aware of market history will be interested to know that both 1998 and 2009 were both bullish and volatile years.

2009 experienced a max early drawdown of -26% in Q1, before gaining +24% to end the year.

1998 started very strong, but experienced a -22% drawdown middle of the year before closing the year with a +27% gain.

This suffices to show that normal and to be expected corrective pullback(s) in the magnitudes of -15% to -25% in 2021 will not be out of context based on historical market behaviour.

VIX Behaviour is abnormal - Flash Correction Indications

The CBOE VIX escalated towards the end of January 2021 to a peak of 37.51, before closing at 33.09 for the month.

The last time VIX hit such levels were during the US election month of October/November 2020.

The excessive speculation in the Options market resulted in a 70% increase in VIX, despite only a S&P 500 drop -2.57% on 27/1/2020.

This excessive speculation occurred due to the recent retail traders collective boycott of heavily shorted stocks by established hedge funds, which is unprecedented. We wrote an article specific to this.

To investigate this further, AlgoMerchant compared the VIX behaviour (since inception in 1990) relative to the S&P 500 and noticed something very interesting.

This is the second time since the 1990s where VIX escalated to a high of 30+% in a single day with a corresponding drop in the S&P 500 in excess of 2%. The only similarity was the February 2018 flash correction which resulted in a peak to trough market drawdown of -11.8%.

There is good reason to be concerned that the recent selldown is showing an unprecedented and dynamic environment that is prone to both flash pullbacks and subsequent rallies.

Which Risk Factors 2021 might be playing out?

In our special 2021 market outlook edition, we highlighted several risk factors to watch out for in the coming months.

| Risk Factor | Analysis | Market Impact |

|---|---|---|

|

Economic uncertainty due to repeat pandemic waves. |

Prolonged recession causing sharp market correction. The longer the recession lasts the higher doubts towards effectiveness of accommodative measures and implementation. Financial conditions will likely tighten. |

Negative equities, oil, basic materials and currencies of commodity exporting countries. Positive USD, US treasuries and Gold. |

|

Increase in defaults |

Tightening liquidity, downgrades and rising bankruptcies will trigger rising defaults. Solvency spikes will be followed by a financial crisis with widespread distress. |

Negative equities, and commodities. High yield bonds default increases. Positive USD, US treasuries and Gold. |

|

Inflation Surprise |

If and when inflation movements start to trend up and achieve the Fed’s target, we will start to see tapering (less accommodate liquidity) as the Fed is primarily inflation data dependent. |

Negative long term US treasuries. Positive Inflation hedge ETFs, Gold. Rotation from growth to value stocks with pricing power that are investment driven. |

|

Emerging Market Financial Crisis. |

A number of countries and events need monitoring for fear of escalation. For example Turkey is extremely delicate with domestic imbalances flashing warning signals. Conflict between India and China over border disputes as well. |

Negative EM equities. Positive USD, US treasuries and JPY . |

So based on available information, are any risk factors occurring?

The answer is yes, we have identified several early warning indicators worth keeping an eye on.

inflation surprise

In Germany inflation surged by a record 1.4% in January (compared to the previous month), after the government removed a temporary sales tax cut and implemented a new green emission pricing scheme.

While an uptick in inflation is what most central bankers will like to see, what is concerning is the fact that german inflation rose more than three times what the economists’ had forecasted.

It would be logical to think inflation surges in one of the world’s largest economies may also be contagion to the rest of the world. While it is still early days for markets in general to be concerned about lock stock and barrel over inflation, it is something we strongly recommend our readers to monitor and be mindful about.

Increasing Stimulus, Waning Economic Growth

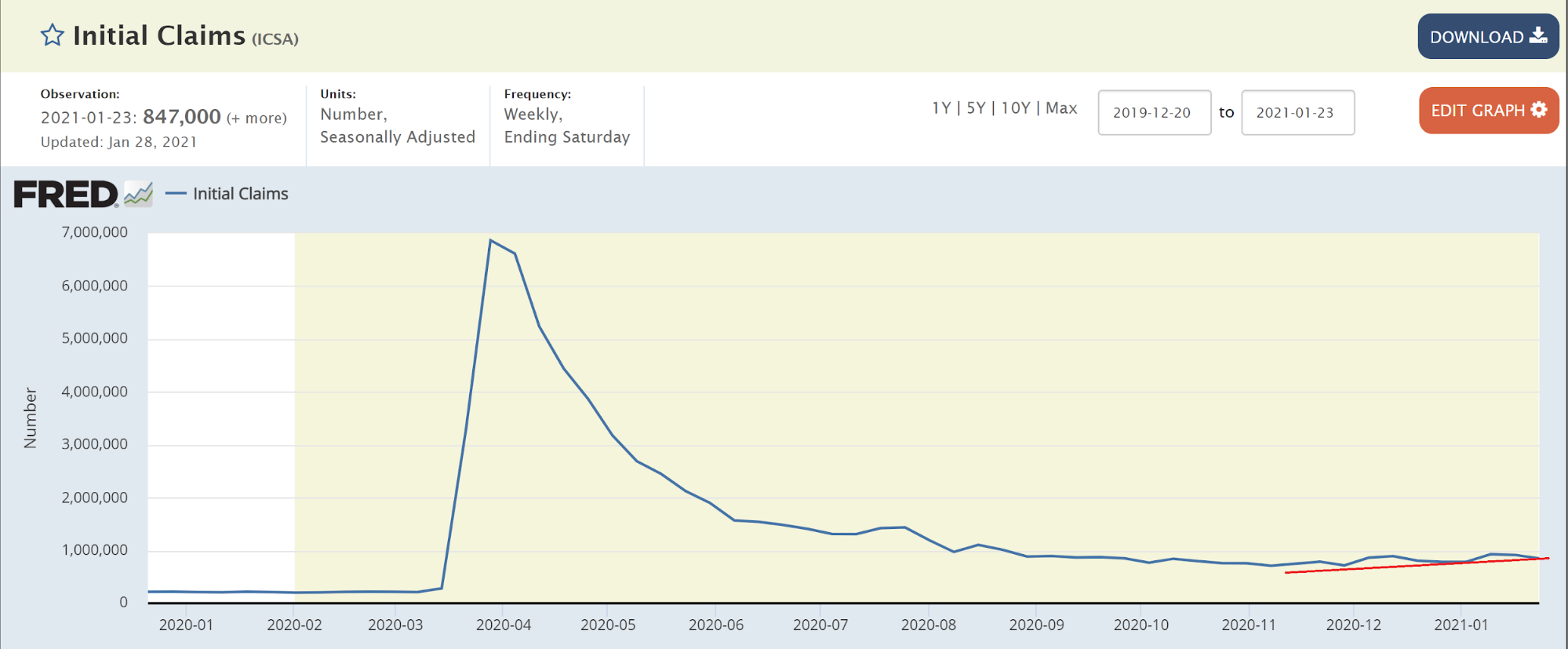

Initial claims is a government employment report that tallies the number of individuals seeking unemployment benefits for the first time.

When a growing number of people willing to work are unable to find work and must resort to claiming unemployment, it is generally a poor sign for the economy.

Since March 2020, initial claims peaked at 6,867,000 due to the Covid pandemic before dropping to the lowest level of 711,000 on Nov 20.

As a reference point, the average initial claims was stable at 200,000 pre Covid.

This indicates the current print of 847,000 is still significantly higher than the pre Covid norms.

Since the low in Nov 20, initial claims have been making higher highs and lower lows, indicating a somewhat concerning outlook.

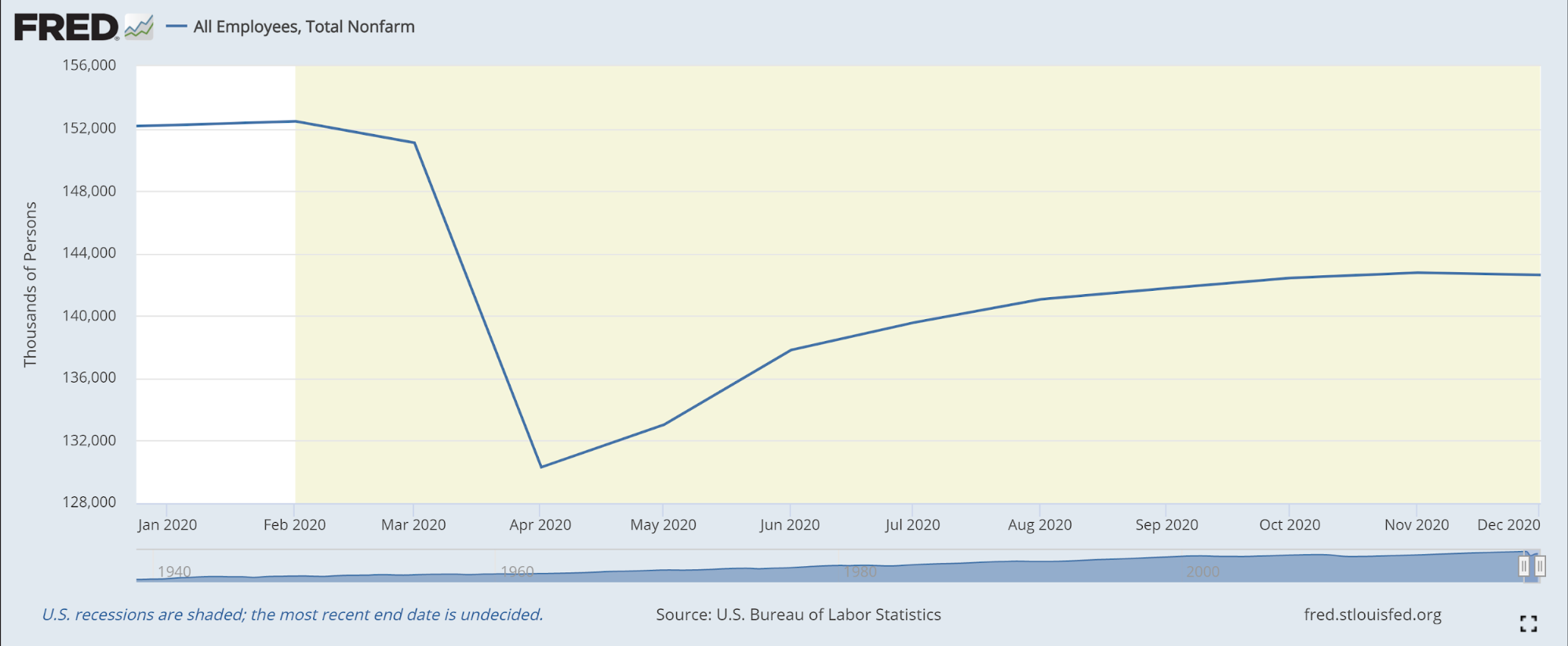

Total Nonfarm, commonly known as Total Nonfarm Payroll, is a measure of the number of U.S. workers in the economy that excludes proprietors, private household employees, unpaid volunteers, farm employees, and the unincorporated self-employed. This measure accounts for approximately 80 percent of the workers who contribute to Gross Domestic Product (GDP).

This measure provides useful insights into the current economic situation because it can represent the number of jobs added or lost in an economy. Increases in employment might indicate that businesses are hiring which might also suggest that businesses are growing. Additionally, those who are newly employed have increased their personal incomes, which means (all else constant) their disposable incomes have also increased, thus fostering further economic expansion.

As a reference point, the total Nonfarm payroll peaked at 152,463 in Feb 2020 pre Covid.

It dropped to a low of 130,303 in Apr 2020, before staging a sustained rebound to a post Covid high of 142,764. In fact, every month since Apr 2020 to Nov 2020, Total Nonfarm payroll had been increasing on a monthly basis.

Dec 2020 was the first time since Apr 2020 where it had decreased.

A decreasing Total Nonfarm can be an indication of deteriorating economic conditions.

Conclusion

The US equities market is showing signs of over-extension amidst a wall of increasing volatility as evident in VIX behaviour caused by the collective forces of retail traders willing to work together.

Truth of the matter is, we are currently experiencing disruption in financial markets. These disruptions have and will continue to change the trading dynamics and market conditions for a long time to come.

So Why are markets selling down? Very simple. Speculative options trading is driving the VIX up. Increased volatility is causing de-leveraging and therefore liquidation of excessive assets.

In closing, where this really matters is the stock market environment has truly changed. Where it has changed principally is we now have an environment that has elevated expectations of volatility in days ahead despite a seemingly bullish uptrend market.