What a year 2020 has been! At AlgoMerchant, we are thankful that we have not only survived, but also thrived to bring our readers and clients new innovations and products in a year so unimaginable and which has taken us all by surprise!

Since it is the start of 2021, we believe that a great way to kick start the year will be to provide our readers with several investment themes that are likely to play out in 2021. These ideas will be shared in this special market outlook edition.

TAKEAWAY

- 2020 was a year that experienced an unprecedented pandemic, Covid-19, followed by an uneven recovery

- This uneven recovery trend is expected to continue even in 2021

- Macro factors likely to drive 2021 are (1) debt and monetary liquidity, (2) Interest rates, (3) Growth recovery rates, and (4) inflation

- Globally these macroeconomic themes will likely play out (1) a more balanced globalisation, (2) growth amidst outbreaks and lockdowns, and (3) synergies between politics, fiscal and monetary policies

- These macroeconomic themes will likely drive these investment themes: (1) rotation into equities, (2) repricing in real estate offering golden nuggets, (3) firm commodities’ prices amidst tepid recovery.

- Risk factors to watch in 2021 are (1) economic uncertainty due to repeat pandemic waves, (2) increase in defaults, (3) surprises to inflation and (4) emerging market stress.

2020 Recap - Unprecedented pandemic, Uneven Recovery

To summarise 2020, it was a year that experienced an unprecedented global virus pandemic, followed by a desynchronised recovery.

Since April last year, after the initial shock of the pandemic resulting in global lockdowns and restrictions, the world started on a very tough but gradual path on recovery. The recovery phase unfortunately has been uneven, and has been constantly dictated by how individual governments and policy holders have reacted to the ebb and flow of the virus cycle.

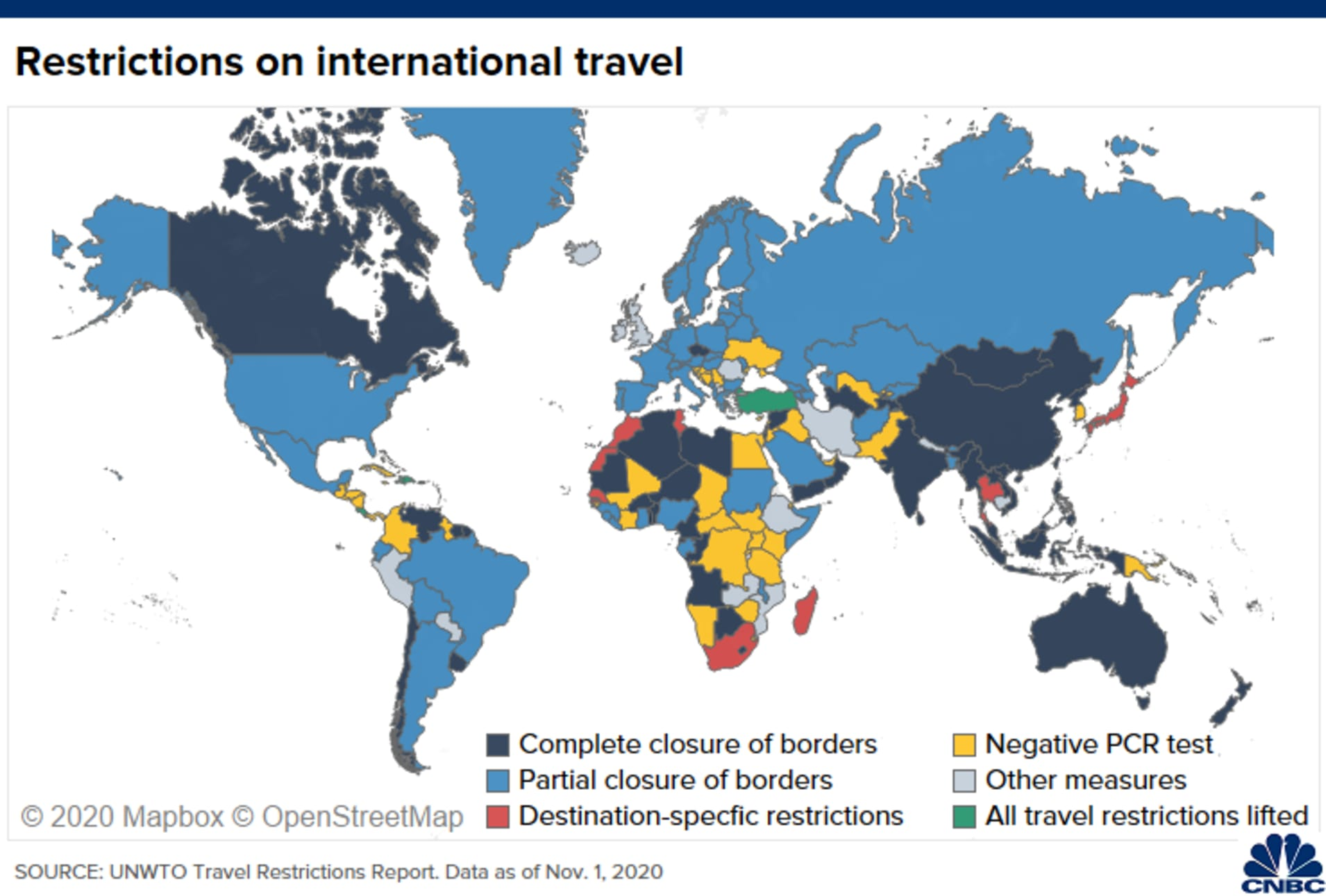

The chart below provides a visual appreciation of how different countries have managed and restricted international travel due to the pandemic. Suffice to say, those that have been the most restrictive are also the ones that have contained the virus better.

Towards the end of 2020, matured economies in Europe and USA had the most lax restrictions on travel, which resulted in them having to bear with the increase in cases and hospitalisation. At the other end of the spectrum were Asian countries like China, Singapore and Hong Kong, which contained the virus very well at the expense of travel restrictions.

This phenomenon of inconsistent approaches in implementing Covid mitigation measures across various countries have resulted in an irregular global recovery that is likely to last into 2021.

What are the consequences of Covid-19?

Global production output, corporate and personal income losses, worsening of income inequalities and the disruption of traditional businesses in favour of online and digital businesses worldwide are the legacy consequences of Covid-19.

It is possible that optimism towards the vaccine in resolving the Covid-19 situation globally within a matter of months is unfounded. It is also very likely that Covid-19 will be here to stay right through 2021.

Virus relapses (which has already taken place) and expectations of continuing monetary and fiscal policies are all within the realms of possibilities.

What are the macro factors likely to influence 2021?

We can expect these economic factors to heavily steer the stock market dynamics heading into 2021 – debt and monetary liquidity, interest rates, growth recovery rate, and inflation.

Debt and Monetary Liquidity

If governments are going to continue issuing more government debt (fiscal), and likewise, if central banks globally are going to inject more money into the financial systems like what took place in 2020, we can expect financial markets to continue to remain accommodative.

If both debt and monetary level maintain at existing levels, with stagnating economic recovery worldwide, the best case scenario is that stock markets may consolidate and trade sideways. However, in the worst case scenario, it could result in significant pullbacks.

Interest Rates

Similar to the above factor, reducing or maintaining interest rates at existing levels will be bullish for equity markets.

If interest rates were increased (refer to the inflation section for potential scenarios), this can be considered bearish for equity markets.

If both debt and monetary level maintain at existing levels, with stagnating economic recovery worldwide, the best case scenario is that stock markets may consolidate and trade sideways. However, in the worst case scenario, it could result in significant pullbacks.

Growth Recovery Rate

In 2020, following the high drop in economic productivity in Q1, the subsequent quarters witnessed significant improvements in numerous economic indicators, such as reduced unemployment rate, recovering GDP growths (MOM), increased production productivity and consumer confidence.

These improving growth recovery metrics also contributed to a V-shaped US stock market recovery.

However, the following scenarios may play out in 2021:

1

Recovery continuation with accommodative liquidity – this is expected to be the best case scenario for equity markets as financial conditions remain accommodative and the results of loose policies are correlated to the economic recovery rate. The US stock market is likely to enter a sustained secular bull run in 2021.

2

Recovery stalling despite accommodative liquidity – this is expected to be less ideal for equity markets as financial conditions remain accommodative but the results of loose policies are not correlated with the economic recovery rate. The US stock market is likely to enter a nordic, range trading phase in 2021.

3

Recovery dropping despite accommodative liquidity – This will be considered a great decoupling whereby abundant liquidity support does not generate recovery growth. The US stock market will likely experience a significant correction in 2021.

Inflation

We’ve provided our views on how inflation can materially change the future market outlook in our previous Special Market Outlook edition.

One key factor contributing to the bullish US stock market is due to the US FED and Federal government printing money to support an economy that has been devastated by Covid-19.

This abundant injection of money at low interest rates to corporations has encouraged significant stock buybacks.

In general, the combination of low interest rates and abundant liquidity is bullish for stock markets. The question is – what can derail this trend?

To answer the aforementioned question, the essence lies in Inflation Expectations. Markets have priced in, and therefore to a large extent, taken for granted low inflation is here to stay. The US FED is desperately trying to nudge inflation upwards to a 2% target where their opine is optimal to spur economic growth, yet not excessively. To do so, lowering interest rates and pumping money are tools at their disposal.

Historically, when the US FED either lowered interest rates or injected money into the economy, inflation would increase. However, since 2008, this classic economic tactic has repeatedly failed to work, which the US FED is mystified and baffled by. This decoupling of inflation reaction from low interest rates and abundant liquidity is hence giving more ammunition to the US FED to pump more money. The net result is a bullish stock market.

If and when inflation movements start to trend up and achieve the US FED’s target, we will start to see tapering (less accommodate liquidity) as the US FED is primarily inflation-data dependent. This will very likely be bearish for the stock market.

Global Macroeconomic themes

A More Balanced Globalisation

The unrestrained trade growth, which was associated with globalisation previously, will gradually decline in light of domestic demand taking centre stage as nations adapt towards self-sustainability. We can continue to expect global trading to remain uneven and patchy. Countries that are particularly reliant on travel, leisure and tourism will be vulnerable. Unfortunately, Singapore is an open country that heavily relies on open borders with limited resources to be self-sustainable.

Countries (China, Europe, USA and Japan) that can generate strongest domestic demand will continue to do well as they find ways to achieve decorrelated business diversifications amidst increased fragmentations and divergence at national levels.

Growth Amidst Outbreaks and Lockdowns

The economic growth and recovery will be dictated by the extension and pace of Covid-19, through future potential outbreaks and targeted lockdowns. This will only further increase divergences across countries.

Asia has been the first to experience Covid-19, and was also the first to successfully contain the outbreak through successful policies and disciplined containment measures.

Thus, we can expect Asian countries to dominate the macro-financial and investment space.

Synergies Between Politics, Fiscal and Monetary Policies

Whether we like it or not, the bar is currently set very high for those in government offices. Policy makers are expected to execute with high efficiency from politics, fiscal and monetary standpoints, to cope with the aftermath of the Covid devastation. This means unprecedented levels of government intervention in financial markets and our daily lives will be here to stay.

Most importantly, this multi-year global push will only result in larger government debt levels. An arduous path to reduce debt quantity, along with its composition and repayment means will eventually be on the cards. The fine balance will be to handle increased taxation to minimise financial disruptions and defaults.

While government debt levels may not pose the highest risk for 2021, it will become a major issue if high debt levels are unable to churn economic growth with inflation escalating.

This will be extremely bearish for equities markets.

Investment Themes for 2021

Rotation Into Equities

The base case for most central banks, governments and major institutions is for liquidity to remain abundant as the global economy outlook remains weak. This is something they can afford to do due to the subdued inflation thus far.

Generally, when liquidity is in abundance, it is less favourable for yield-related investments and more favourable towards equities. Expectations are for equities to present a better risk-reward profile going into 2021.

To furnish more details, upside for yield related investments will likely be capped due to spread tightening, whereas equities will have room to outperform even further, especially if profits were to surprise on the upside with listed companies providing stellar forward guidance.

Real Estate Investing – Look for Golden Nuggets Amidst Repricing

The evolving context of the Covid-19 crisis has resulted in global commercial real estate markets experiencing significant declines in deal activities. While low interest rates should support real estate recovery, we can expect significant repricing of real estate. This repricing is expected to provide opportunities in the following real estate sectors:

1

Logistics – Logistic real estate has benefited tremendously from high e-commerce activity. In particular we should expect to see higher demands for industrial warehousing and logistical properties. Given the experiences gathered from handling the pandemic, we can expect multi-channel retailing to become common practice. This will likely drive logistic properties to become even pricier while physical retail store locations may no longer command the prices they used to have.

2

Hotels – This industry will be the last to recover from the hotel pandemic since it is highly correlated to the travel industry. With air travel being restrictive at least until before the majority of the global population is sufficiently vaccinated, the hotel property industry is likely to remain suppressed. However, since the stock market is always forward-looking, there will be opportunities to identify and pick up beaten down hotel-related stocks in 2021.

3

Offices – We can expect the office sector to primarily be focused on core assets, especially the best quality office assets. The reason why best quality office-related REITS and stocks will likely do well can be attributed to stellar firms with long-term leases that are able to adapt to social distancing yet operate with a mobile workforce complemented by technology. Remote working will likely remain the norm and may even accelerate. However, strong core businesses that demand strong corporate culture and team building will mostly retain their office premises.

Commodities – Firm Even With Tepid Recovery

The outlook will remain positive for commodities, even though global recovery remains volatile and vulnerable. Historically, commodities are highly sensitive to economic growth, inventory, production supply and demand forces, and assumptions. However, financial conditions have also impacted this asset class in recent years, just like others.

On top of the global economic recovery, currencies and more recently supportive reflation attempts by central banks’ monetary policies have also become important factors in driving commodities’ expectations (especially precious metals and gold).

1

Oil – WTI is expected to trade within range of $40-50 due to sustained demand forces associated with pickup in demand and the active OPEC+ supply management.

2

Base Metal – Covid-19 significantly affected base metals in 2020. Copper, Lead, Tin and Aluminium remain significantly undervalued heading into 2021, especially with strong support from China’s growth and a rebound in manufacturing and building construction from depressed levels.

3

Gold and Precious Metals – Easy money from central banks due to economic uncertainty will remain key drivers for gold and precious metals. Current economic conditions should help real rates maintain at existing levels, which will assist gold to head higher. The combination of a vulnerable recovery, weak dollar, strong chinese yuan are supportive factors.

Risk Factors to watch in 2021

| Risk Factor | Analysis | Market Impact |

|---|---|---|

|

Economic uncertainty due to repeat pandemic waves. |

Prolonged recession causing sharp market correction. The longer the recession lasts the higher doubts towards effectiveness of accommodative measures and implementation. Financial conditions will likely tighten. |

Negative equities, oil, basic materials and currencies of commodity exporting countries. Positive USD, US treasuries and Gold. |

|

Increase in defaults |

Tightening liquidity, downgrades and rising bankruptcies will trigger rising defaults. Solvency spikes will be followed by a financial crisis with widespread distress. |

Negative equities, and commodities. High yield bonds default increases. Positive USD, US treasuries and Gold. |

|

Inflation Surprise |

If and when inflation movements start to trend up and achieve the Fed’s target, we will start to see tapering (less accommodate liquidity) as the Fed is primarily inflation data dependent. |

Negative long term US treasuries. Positive Inflation hedge ETFs, Gold. Rotation from growth to value stocks with pricing power that are investment driven. |

|

Emerging Market Financial Crisis. |

A number of countries and events need monitoring for fear of escalation. For example Turkey is extremely delicate with domestic imbalances flashing warning signals. Conflict between India and China over border disputes as well. |

Negative EM equities. Positive USD, US treasuries and JPY . |

Conclusion

Marked by the most devastating recession in recent history, 2020 was really an unprecedented year worthy for the history books. With the Covid-19 pandemic is not showing signs of abating globally, we enter 2021 marked with continued uncertainty, although the outlook remains mildly positive with expectations for the path to pre-crisis growth levels to remain long.

Against this background, there are investment opportunities to be made, with flexible and nimble play being a key strategy due to market participants clearly favouring rotation in cyclical themes.

Keeping a strong focus on quality and being willing to pay a premium for high quality stocks within popular cyclical themes may be necessary in an uneven recovery market.