Wall Street faced sharp losses as fears over new U.S. auto tariffs rattled investors. Tech and auto stocks led the decline, with Nvidia and Tesla seeing significant drops. The S&P 500 fell 1.12%, while the Nasdaq tumbled 2.04%, reflecting growing market uncertainty.

U.S. stocks rose, led by Tech, Consumer Goods, and Telecom, despite mixed market breadth. Fed policy and tariff concerns may impact stability, but inflation control efforts could aid recovery.

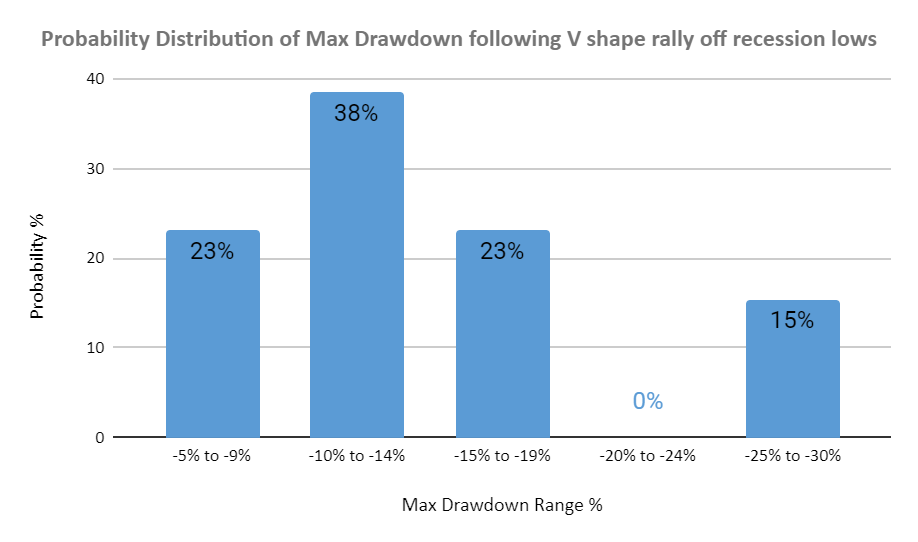

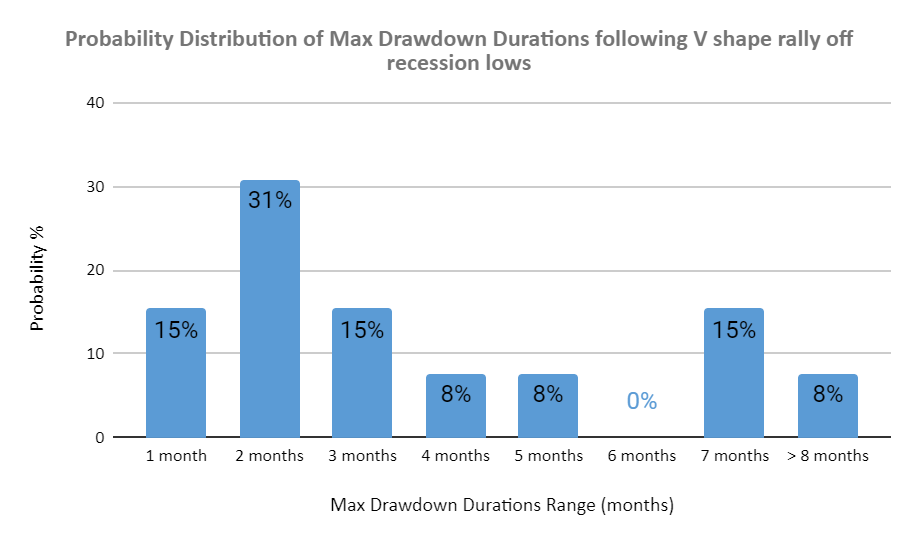

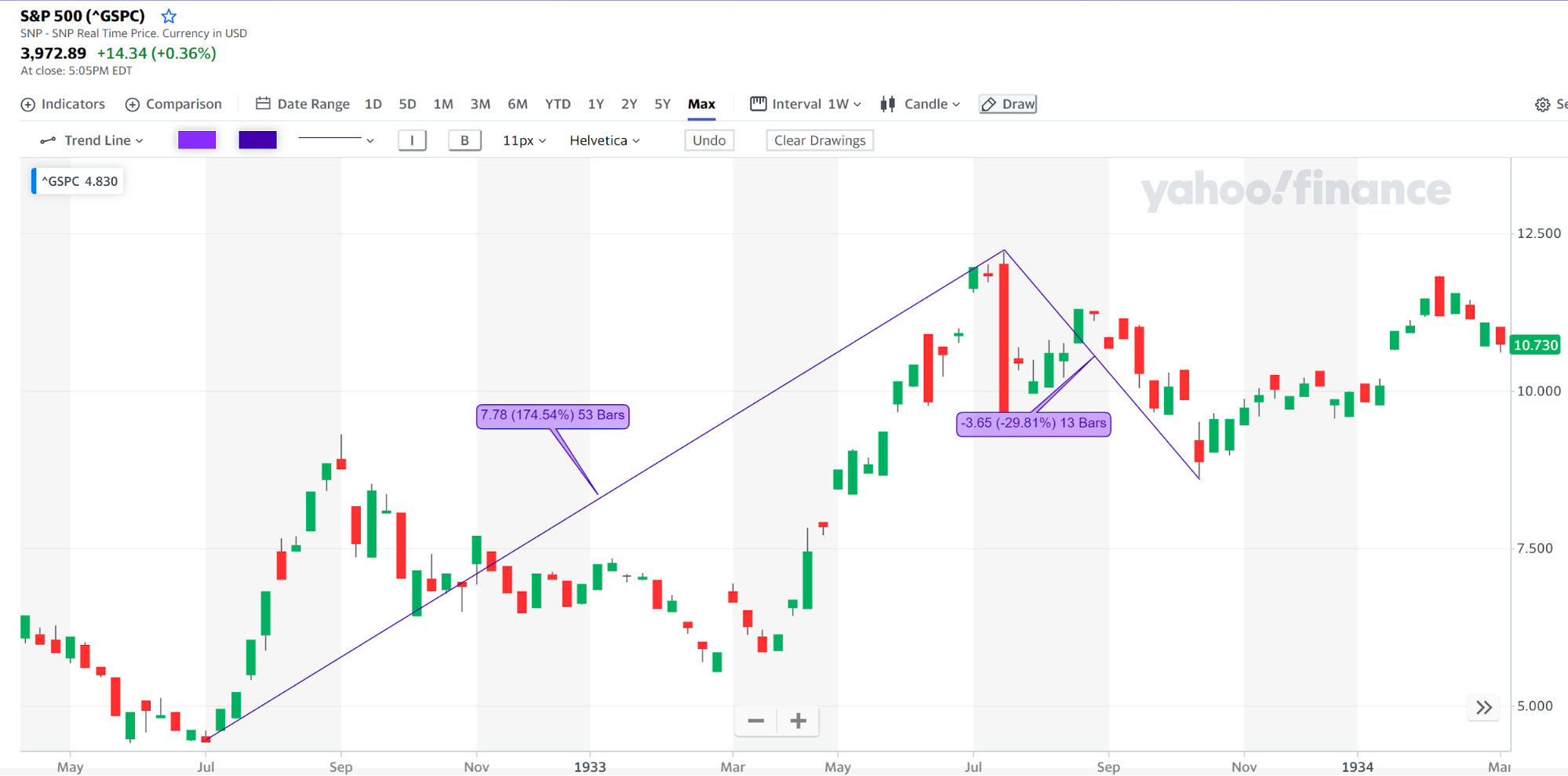

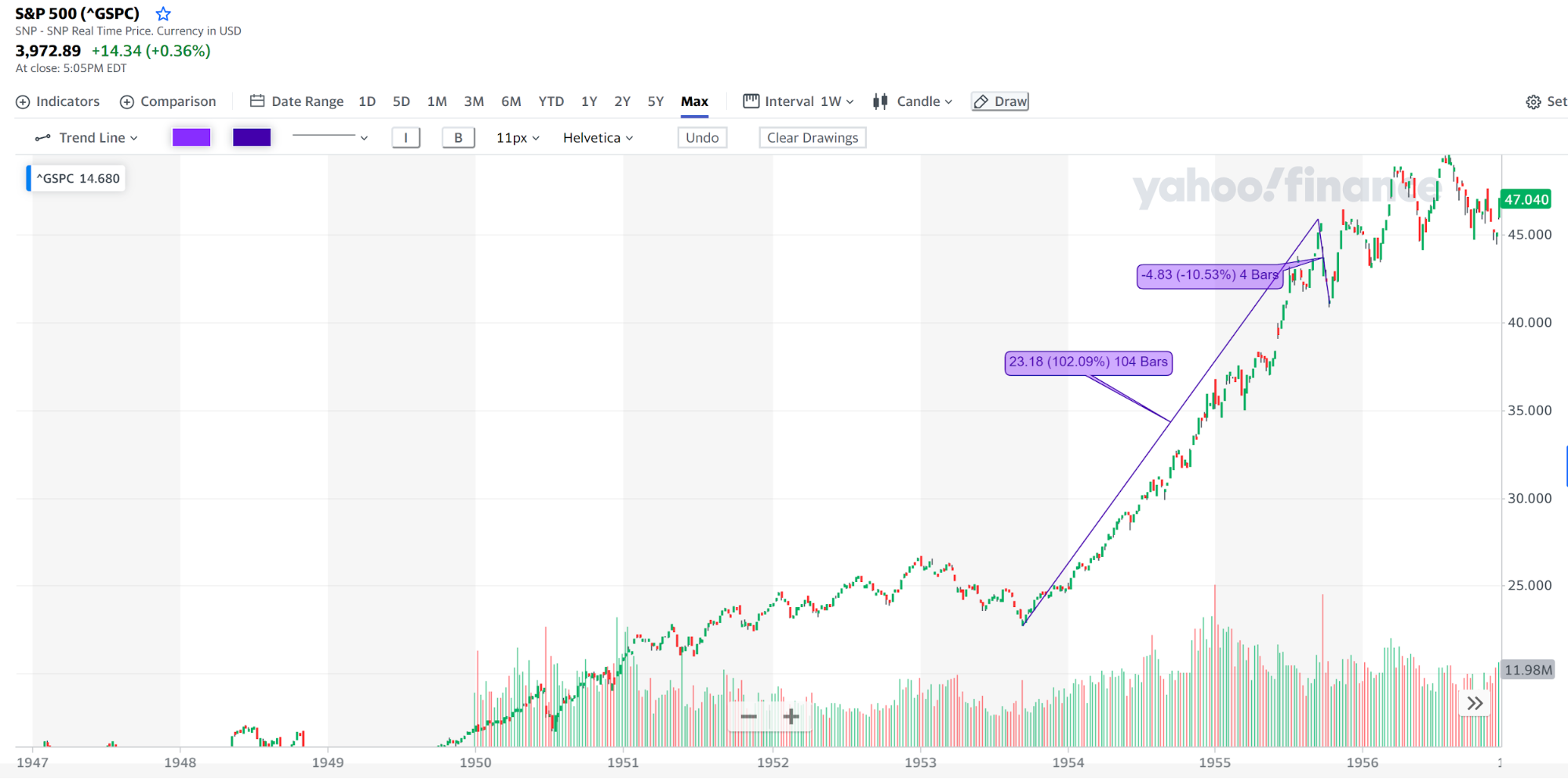

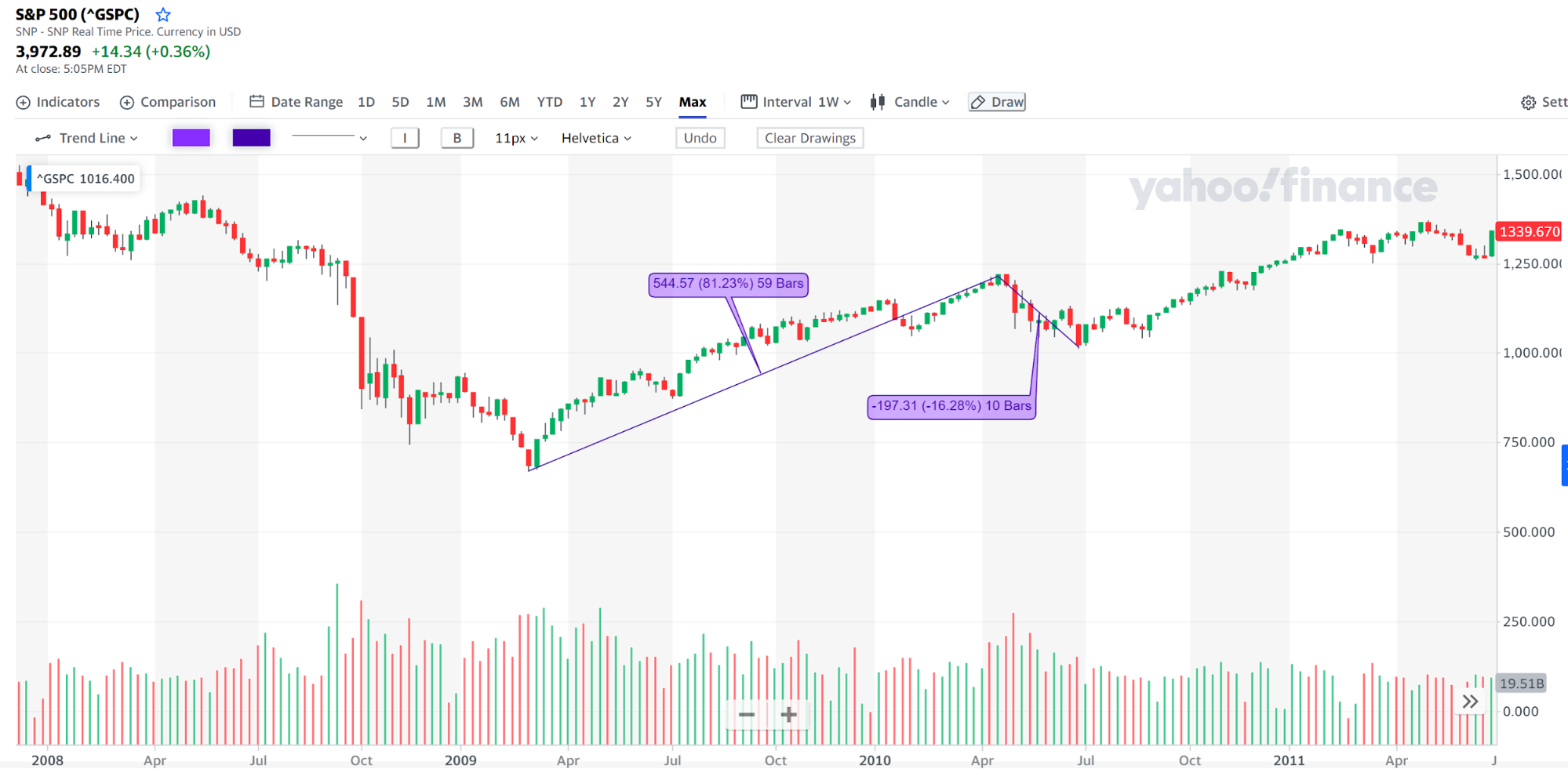

S&P 500 Plunges—Will This Be a 20% Rebound or More Pain Ahead? 🚨 The market has officially slipped into correction territory, dropping over 10% from its peak and leaving traders at a crossroads. Hold, buy the dip, or cut losses? History reveals a shocking truth: the first week after a correction can dictate the market’s fate for months. In this episode of Smart Money Insight, we uncover the hidden signals to watch next week, and whether a massive rebound or further decline is on the horizon. Don’t miss this critical breakdown!